What is Structured Trade Finance (STF)?

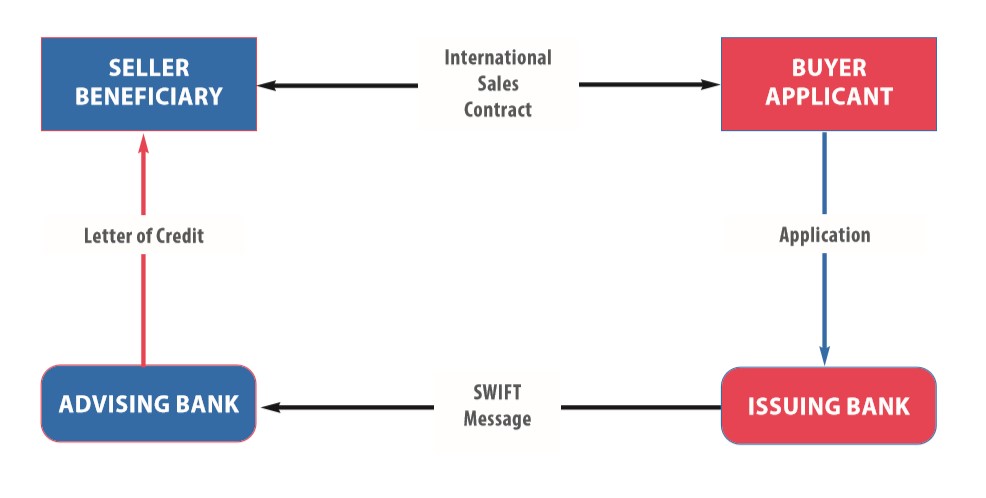

Structured Trade finance (STF) represents monetary activities related to commerce and international trade. Trade finance includes the issuance of documentary letters of credit (DLC), factoring, export credit and insurance. Companies involved with trade finance include importers and exporters, banks and financiers, insurers and export credit agencies, and goods or service providers.

The function of trade finance is to introduce a third-party to transactions to remove the payment risk and the supply risk while providing the exporter with receivables according to the agreement and the importer with extended credit. Suppliers, banks, syndicates, trade finance houses and buyers all provide trade financing. Ametheus helps bring all of these pieces together through our technology and support services, ensuring effective funding and settlement of trade finance commitment over the life of the financing agreement subject to applicable terms and conditions formulated by our in house finance team.

What we do?

Ametheus Holdings Pvt Ltd is a structured trade finance service aggregator or introducer, not a lender, working with Limited Companies and Incorporated Bodies who may pay us a commission. Our goal is to engage genuine Buyers and Sellers of various commodities and to provide them Letter of Credit facilities. We are a facilitator not a lender, working with selected companies. Our product line offers a variety of leased products from the top financial institutions. What we offer are for corporations in B2B basis who require credit line to import commodities.

We assist companies to structure import credit line. While we can access many traditional forms of finance, we are specialized in alternative finance and complex funding solutions related to international trade. We help companies to structure import finance in ways that is sometimes out of reach for mainstream lenders. We arrange LC for client’s supplier upon a deposit margin depending on commodities and a service fee which varies depending on amount and tenure of LC.

Our extensive connection with premier business houses powered us to organise Letter of Credit from the top of the line banks with validity of 90-180 days. We arrange LC for client’s supplier upon a deposit of refundable or adjustable margin amount depending on commodities and a non refundable service fee which varies depending on amount and tenure of LC. Client requires to settle the balance payment and charges 7-14 days before the shipment arrives at the destination port.

Products we cover:

We can issue LC for such kind of commodities which have a market based price index. We prefer LC for following products:

Scrap

Metals & Minerals

Coal

Building Materials

Chemicals

Agri Commodities

Petroleum Oil

Visualizing a letter of credit transection

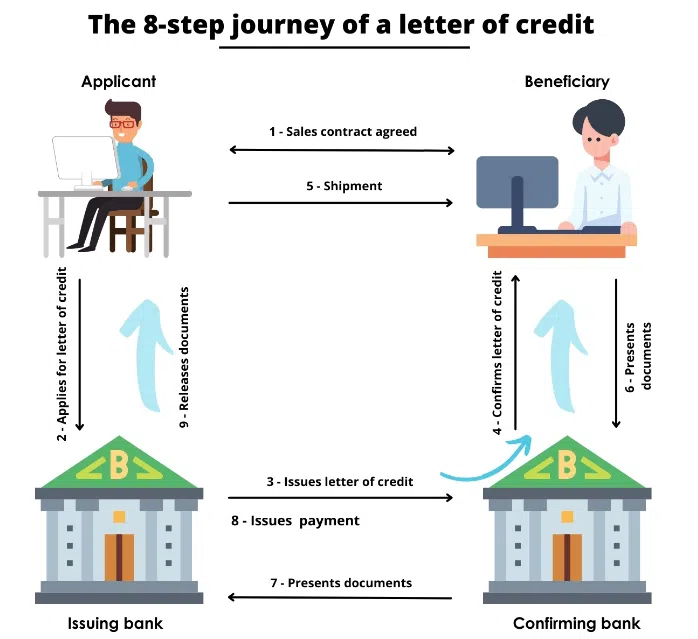

For reference, the following are our issuance procedures:

1. Client submits a proforma invoice (PI) or Application Form for the underlying deal.

2. Ametheus (our firm) creates a draft and issuance PI for client’s review.

3. Client signs the draft, wires issuance fees, and submits due diligence documents.

4. Ametheus releases the instrument to Bank for issuance.

5. Assuming no questions, Bank issues SWIFT within 5-15 Days maximum.

6. Ametheus emails a copy of SWIFT to client.

Import Finance Workflow:

A. LC applicant will open LC on behalf of importer to the exporter (LC Beneficiary). After shipment against documents LC applicant will issue acceptance subject to conditions basis.

B. Containers will arrive in port with 30 days free detention. Containers will be booked by the exporter (LC Beneficiary) or shipper.

C. Shipment Documents will be sent to the importers or consignee’s bank on 45/75 days DA basis depending on the usance period and validity of the LC. So, the ultimate importer can collect/retire documents from bank and can release containers.

How the Transaction Will Work:

A. LC applicant first will open LC.

B. Usance LC can be issued with 60 days Usance with 30 days validity or 90 days usance with 180 days validity. At sight LC can be issued with 90 days/180 days validity.

C. Beneficiary of LC or exporter will make shipment.

D. Beneficiary or exporter will submit documents in his bank .

E. Beneficiary bank will send documents to LC applicant’s bank for acceptance against documents.

F. LC applicant will issue acceptance of payment at sight or will give acceptance that on the maturity date (last date of the usance period) LC issuing bank will pay .

G. LC applicant will send documents to the consignee’s bank asking for acceptance .

H. Consignee’s bank will issue at sight payment to LC applicant’s bank against the documents or they will also send acceptance of payment to LC applicant’s bank that on the maturity date (last date of the usance period) they will pay LC applicant’s bank and then importer’s/ consignee’s bank will finally release the documents to consignee.

Benefit: Importers can import without engaging FDR or limit. Exporters can recommend importer to utilize this LC facility.

LC at Sight

A sight letter of credit is a document which stands as a proof of payment in return of the goods or services to be released for the transportation by the seller. Once the goods or services reach the buyer, the buyer has to pay the financial institution that provided the Sight LC.

The process of submitting and verifying the documents is known as the sighting process, after verification the document is called the Sight LC . The banks or financial institutions generally take between 5 to 10 business days to process these documents.

Under LC at sight exporters have freedom to manage their working capital as they can receive payments against goods as soon as the shipment is on the way, which is one of the most beneficial benefits of a Sight LC. As a result, the exporter may not encounter a cash constraint and can effectively manage working capital.

We can issue at sight LC in 7-14 days.

How does a Sight LC work?

Step by step process of how sight letter of credit works:

-

- A buyer who needs certain goods contacts a supplier and gets a quote for the requirement and confirms the deal.

- The buyer then goes to his bank, generally, one that has already extended him a line of credit and asks the bank to issue a sight LC towards the supplier.

- After having looked at the creditworthiness of the buyer, the bank issues a sight LC and sends it to a bank in the supplier’s country.

- The supplier’s bank then informs the buyer and sends them the LC along with all the terms and conditions of the trade.

- Once the supplier is happy with the LC, he ships the products and submits the shipping documents to the supplier’s bank.

- The bank processes the documents and sends them to the buyer’s bank.

- The buyer is alerted by the bank that the documents have arrived, and he needs to make the full payment to collect the documents. The buyer will need these documents to get the delivery of the product.

- The buyer inspects the documents and pays for the LC, after which the buyer’s bank sends the payment to the seller’s bank. The seller is paid for the amount, generally much before the goods reach the buyer.

LC at sight – Payment Terms

When a bank issues a sight LC, it acts as a guarantor of payment to the beneficiary. The seller has to furnish all the shipping documents mentioned under the terms and conditions in the LC to receive the payment. Once you submit all the documents and the issuing bank verifies the same, the bank releases the funds. The buyer immediately makes the full payment to the bank upon the receipt of documents.

In case the supplier is not able to provide the documents, the bank is not liable to release the payment. Furthermore, if there are any discrepancies found in the paperwork, the issuing bank can deduct a small fine from the total payment.

By now you’d have come to the realization that trade finance is a complicated subject that exporters/importers have to deal with on a regular basis simply due to the complexities involved with international trade.

At Ametheus, we understand the plight that most importers are faced with and our competitive exporters finance products & buyer’s credit products are best suited to facilitate hassle-free international transactions so you can focus on scaling your business.

Usance LCs

In the case of Usance LCs, also known as deferred payment LCs, the buyer is given a grace period of 30, 60, 90, or 120 days after receiving the documents to make the payment. This is known as LC 30 days, LC 60 days, LC 90 days, and LC 120 days.

Under usance letter of credit the buyer is allowed to make the payment after the delivery, within a stipulated grace period. Unlike with sight LCs, the buyer doesn’t have to make payment immediately to receive the documents. Usance LCs generally provide a buffer of 30, 60, 90, or 120 days to make the payment. A usance LC is also known as a deferred payment LC, or a term LC.

Benefits and Drawbacks of Usance Letter of Credit

-

- The buyer, who is given a credit time to complete a payment, benefits most from a usance letter of credit. No other kind of letter of credit provides the buyer with the option of postponed payment. For the buyer, this translates to operating money without interest.

- Additionally, better working capital management is the outcome. The buyer may obtain the items before completing the payment when utilising a use letter of credit, which is another crucial factor to consider. He can then inspect the things before paying for them in this manner.

- However, the identical set of benefits turns into a negative for the seller. As he extends a credit duration to the customer, the seller must manage his strained working capital.

- In conclusion, a usance letter of credit is typically utilised when the purchaser has the advantage over selling or when the property exists. The seller consents to abide by the mild conditions of an overdraft Usance letter of credit.

Advantages of Usance LC for the Exporter

-

- The discount bank will provide the exporter with immediate cash.

- Daily Sales Outstanding (DSO) is decreased when payment is received “at sight”.

- This LC makes things more marketable by offering customers the perk of more extended payment periods.

- Maintains the price’s integrity because the seller need not factor in the expense of covering more extended payment periods.

- Maintains the integrity of the receivables since the letter of credit continues to provide security for payment assurance.

- Allows for more extended payment periods and the possibility of less expensive financing, strengthening ties with customers.

Advantages of Usance LC for the Importer

-

- Comparatively speaking, borrowing is cheaper than any other kind of financing.

- It facilitates working capital optimization.

- Payment deferral for a maximum of 360 days

- Foreign money can be purchased at a discount rate.

- This approach is straightforward and practical.

- This LC allows for payment upon Sight, which improves ties with the supplier.

- Days Payable Outstanding (DPO) is enhanced by offering more extended payment periods.

- It aids in providing a second source of cash.

FAQ:

Q: How will the importer get the product and how will the importer pay back to you?

Ans: DA means documents against acceptance. So, when the importer’s bank will receive documents, they must issue acceptance to LC applicant’s bank to release the BL copy from the bank to release the containers. In that way LC issuing bank will get payment from the importer’s bank against the acceptance they gave to retire the documents.

Q: What is the security of the importer?

Ans: Consignment is coming in the name of importer or consignee, so the transaction is secured. Additionally, importers can take business insurance coverage from Allianz Trade (Euler Hermes) or Coface through us.

Q: What volume can you do?

Ans: Minimum 200,000 USD to any amount of LC we can arrange.

Q: Any Hidden Charges?

Ans: Only one hidden charge is money movement charges which is negligible and on actual cost basis.

Q: Who will do the quality inspection?

Ans: SGS, Bureau Veritas, Cotecna etc.

Q: Who are the parties here?

Ans: LC applicant is financier and notify party. Exporter or shipper is LC beneficiary. Consignee is the ultimate importer. Ametheus Fintech & Offshore logistics Pvt Ltd is the facilitator of this entire transaction.

Q: Are there any upfront charges?

Ans: Client must pay LC issuing charges upfront.

Q: Which products are allowed to do?

Ans: Commodities and other non-perishable items which has index basis price indication and less price fluctuation in the market.

Q: How long may a Usance letter of credit start opening?

Ans: Usance LCs often offer a repayment grace period of 1,2,3, or 4 months. A period LC or a promissory note LC are other names for a usance LC.

Q: Can LC from a user be forwarded?

Ans: Only when it is mentioned explicitly in the LC that the LC is transferable then LC can be transferred by 1st beneficiary to 2nd beneficiary.

Q: Can we reduce the usance of LC?

Ans: The exporter is given the option of a Letter of Credit Discounting for the Usance LCs. In a typical business transaction, the buyer requests a credit term while the seller requests prompt repayment. To resolve this conflict, the bank assists the export using LC discounts.

Q: What does LC payable at Sight mean?

Ans: Usance Credit Current liabilities at Sight is a type of L/C in which the exporters perform sight collections from the cheque drawer, which handles the discounted, and the importation pays advanced payments to the financial institution, which provides financing for the importation.

Q: On some exchange bills for usance, who is responsible?

Ans: A usance bill of exchange needs to be paid in the future, such as in a few days, weeks, months, or years, such as “3 months sight.” To hold the payee accountable for the payment, he must accept it. By stamping on the front of the bills, the payee acknowledges it and swears to pay it when it matures.

Q: Why LC issuing bank issue acceptance to seller?

Ans: LC acts as an irrevocable guarantee, If the buyer is unable to make a payment, the bank covers the full or the remaining amount on behalf of the buyer. The Issuing bank has to confirm to the negotiating bank about the acceptance / payment of the documents for reinstatement of the amount in the LC.

Q: Can sight LC be discounted?

Ans: Sight letters of credit should not require any discount mechanism as issuing banks or confirming banks must honour at sight credits as soon as they determine that the beneficiary’s presentation is complying.

Q: What is the maturity date for Sight LC?

Ans: Sight LC matures on the date on which the documents are submitted to the bank by the beneficiary.

Q: What is the maturity date for Usance LC?

Ans: Usance LC matures on 30, 60, 90, 120 days from the date on which the documents are submitted to the bank by the beneficiary.

[email protected]

www.ametheus.com